“And we’ve won let me tell you we’ve won.”

This was Trump’s victorious proclamation early on in the war that has recently been opened on Iran. After a number of days we then heard a somewhat more modest, “We’re winning.” And many days after that, at the time of writing, the war has entered its fourth week and Iran is sending sophisticated missiles into Israel, and not all of them are getting intercepted. In short, we launched an undeclared war (along with Israel) with a maximum of military might, but also with a maximum of overweening optimism and bravado (at least on the part of the administration). The term hubris comes to mind.

Unreality As a Symptom of The Decline

A major theme of American society is unreality, which here refers to the tendency to retreat into fantasy and delusion. It can be argued that this trait has been a salient feature of America for quite some time; as Kurt Andersen writes in Fantasyland – How America Went Haywire, it was there at the very beginning of the country’s founding (forget Pilgrims and religious freedom, at first it was all about gold and riches). I would further make the case that this trait becomes heightened during the phase of Decline, as the “good times” of the Rise and Top begins to slip away and fade into “image” (i.e. to become a simulacrum of “good times”). It’s a sort of “digging in one’s heels” against encroaching reality. A process that is currently unfolding.

This unreality pervades all aspects of life in America, from the top “leadership” (in quotes to denote something more like a parody of leadership) to the economy to everyday life. Following is a broad sketch of the scope of unreality in a myriad of guises, organized as a series of topics (each one itself a sketch, intimating much larger discussions). Since the post began with the Iran war, the first deals with various examples of unreality in the American Empire.

The Unrealities of the American Empire

Foremost is the belief of omnipotence. This is backed up by the largest and most advanced military on the planet, backed by all manner of technological advances. Yet, despite these advances, limits remain. Going back in time, the US possessed all sorts of major technology in such wars as Vietnam and Iraq (Iraq 2.0), but despite all the massive destruction (and all the people – noncombatants – that were killed), a decisive victory remained out of reach in each case. (Both incurring incredible amounts of money btw).

Another aspect of omnipotence is the fact that the US dollar is the world’s foremost reserve currency. There are many benefits that flow from this situation, not least being it helps making many goods and services cheaper than they would otherwise be (will not go into this – see Dalio for example).

The United States used to be framed in terms of exceptionalism. It wasn’t just our military might and gigantic economy, there was a moral dimension to our place in the world. America was, for example, a prime force behind the expansion of Democracy throughout the world. This and other virtuous projects were the basis of the so-called City on a Hill narrative. But there has been a shift over time, and which has accelerated under the Orange Guy. So that our might has devolved into a kind of brutish version, solely in terms of our military and economic might.

It could be added that hiding behind narratives of exceptionalism are all manner of examples of the United States acting in aggressive and cruel manner, taking on other countries directly, such as Spain in the late 1800s and Iraq more recently. Or meddling in the affairs of other countries; one prime example being Chile in the 1970s, when we decided nationalizing resources was a threshold we would not tolerate… leading to a bloody coup led by a brutal general. The sort of person the OG seems to show deference toward (Putin, Xi, etc).

Without exaggeration it can be said the United States is richest nation on earth, and for that matter in all of history. At one point some decades ago we could boast a standard of living enjoyed by most Americans unparalleled in history and among even other developed nations. Included in this was the substantial percentage of households that were solidly middle class. But now there has been a shift. For one, the vast wealth of America is extremely unevenly distributed, as graphed in this chart from Wikipedia (there was a nice chart from Statista that is no longer available without an account). This chart (Q1 2024) shows that the top 10% hold 67% of total wealth in the US. The middle class has shrunk (since the 1970s), and really, given high costs for things such as housing and healthcare, only the upper middle class can realistically be considered middle class (much of the middle class is really working class at this point). Note the bottom 20%’s meager portion. This situation is a segue into the following topics.

Potemkin Economy

Besides a “real” economy of production of goods and services there is a kind of parallel economy that is a matter of narrative – the economy as spectacle. In this spectacle economy vast wealth is being created: the “pie” keeps on growing and everyone (households) enjoys a generous portion. This is a version of The Mirage. The truth is, though, we know that many are finding themselves looking at a pretty miserable slice of that “pie” on their plate (see reference to the bottom 20% above). And there are other issues concerning this narrative.

The common metrics hide the true reality. GDP, for example, is in large part based on consumer spending (PCE – Personal Consumption Expenditures): roughly two-thirds of all economic activity. The first thing to note is that PCE has a larger share than production. But there is a further issue in terms of consumer spending, with an estimated 50% of this spending coming from the top 10% income tier. (TO DO – ref to more detailed analysis, with maybe a link)

We keep on hearing how the labor market is still considered “robust” and “resilient,” which is taken, with labor used as a proxy for the economy, as proof the economy is in good or even great shape. Look at the unemployment rate! At around 4.3% that is historically pretty low. Except… we know a lot of people are struggling, and concerned about the job market. The Ludwig Institute for Shared Economic Prosperity has an interesting analysis of this situation that includes the notion of being “functionally unemployed.” This is a category that not only includes those currently looking for a full-time job but also those whose income fails to reach an adequate threshold enabling them to adequately pay for basic necessities such as housing and food; in other words a living wage. Currently LISEP estimates that a worker must earn at least $26,000 before taxes to be considered earning a living wage (however, some areas/cities/etc require a higher amount).

There is another dimension to current economic activity that involves spending on AI; to be precise, spending on AI infrastructure such as data centers. This is not the place for an in-depth discussion, but suffice to say there are a number of problems related to these data centers; energy and water consumption are at the top of the list. But this activity has a misleading aspect, seen in the large amount of circular financing involved, where much of this activity involves an AI-related company pouring money into another one. Big tech companies such as Nvidia and Microsoft invest tons of money into AI firms such as OpenAI and Anthropic, which in turn use that money to buy hardware and cloud services from those investors. This looks good on paper (jacking up the GDP). Also to be noted is the staggering amount of debt involved, so that some companies are now seeing negative cash flow. In recent months Oracle and Microsoft have gotten hammered in the stock market as some investors basically freaked out on the level of debt involved… with no substantial revenue in sight (derived from their AI projects). I could go on, but AI, being touted as a kind of miracle. A miracle that at the moment is not really yielding spectacular results based on spectacular amounts of debt.

Wealth

America proclaims itself as the richest nation in the world. On the face of it this is true but there are some problematic aspects to all this “wealth.”

First, there is the large wealth inequality already alluded to. This can be seen in such comparisons as: the top 1% (that’s ONE percent) has a net worth of about $52 trillion, vs the bottom 50% (half of all households) has a net worth of only something like $4 trillion (data from Fed Reserve and other sources). Further, much of that $4 trillion is based on value of the homes owned by this group (problematic given the moribund state of the current housing market).

This vast accumulation of wealth by the top 10% or so translates into outsized leverage of political power (i.e. see Turchin’s work). In other words this large disparity is a major force shaping American society, in many instances in ways not widely reported on, not least in the media itself; this would include the shrinking number and variety of media venues. It appears there are now just a handful of large corporations – in tandem with billionaires – who control the majority of media (controlling what is, what is not, and how things are, reported).

But there is a more subtle issue nature of this wealth, and that is much (most) of this wealth isn’t actual money, but assets. Although there are some assets that are tangible, such as real estate and precious metals, much of it now is intangible. It is really a matter of abstractions, numbers in bank ledgers/computer systems. Such wealth can be converted to money. But it is not cash sitting around in bank vaults. This wealth increasingly is the result of speculation – and that is why I constantly put quotes around the word. See Ray Dalio for example for a fuller description of this.

Magic Money Machine

Aka the Big Casino.

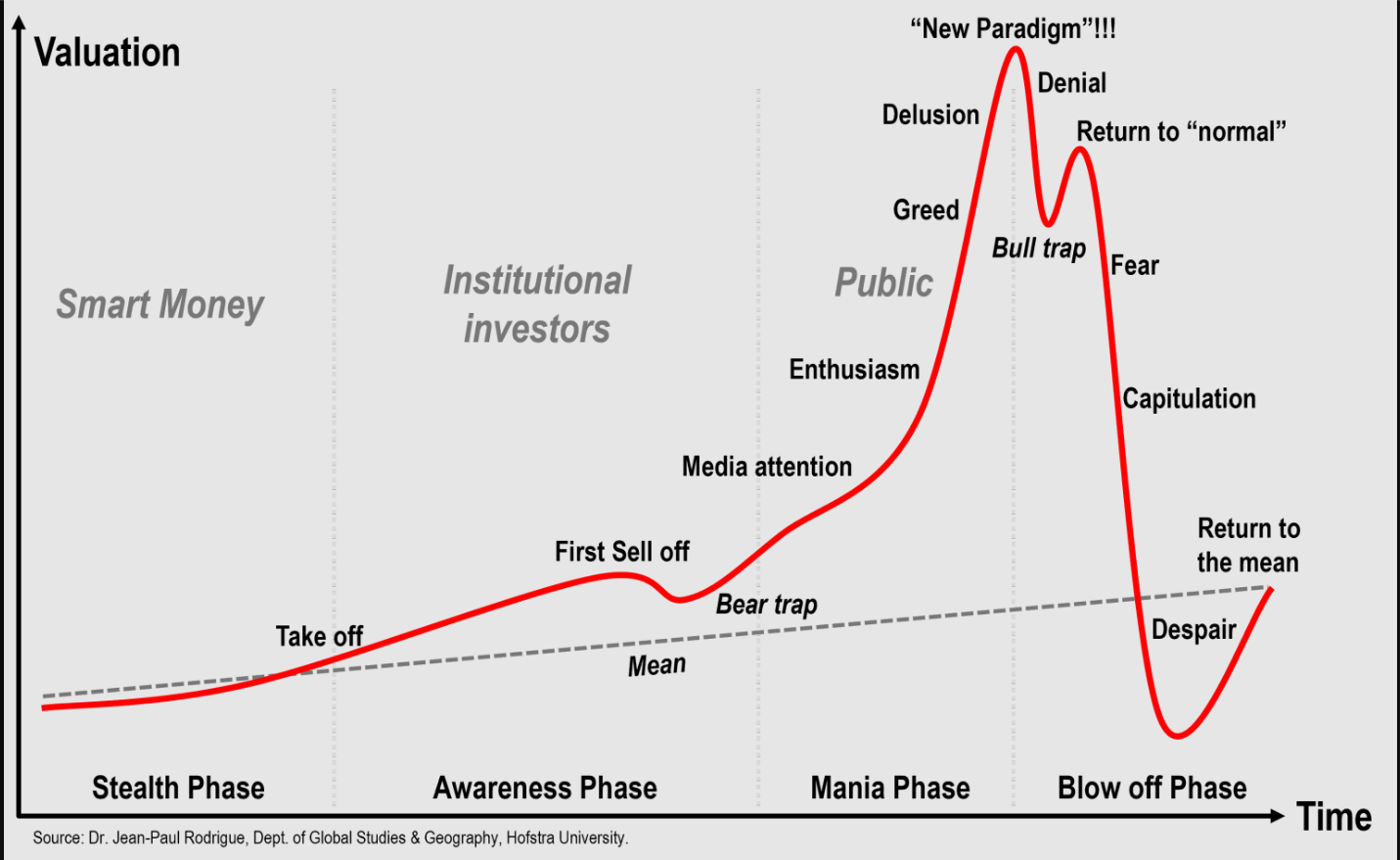

Given the already overwhelming territory being covered, only a few points will be mentioned regarding the stock market and the vast “wealth” it represents. The previous description carries over here. With stock prices now at valuations that have become completely disconnected from the “real” economy.

This disconnection can be seen in various metrics, one of the simplest is the so-called Buffett Indicator. It is not hard to understand: it is the ratio of total market capitalization and the GDP. It’s not fully predictive, but a kind of broad indication as to the overall state of the market. It shows to what degree the market is outpacing the economy. And currently, this ratio is seeing values that have never been seen before. With recent values at 215% to 230%, the market is well above double the valuation of the actual economy. It means there is a large amount of speculation, rather than production of actual goods and services. The economy quite simply is not yielding monetary returns that come close to current valuations.

And central to this speculation is of course the current mania over AI. This has already been alluded to. But again, a large group of overly optimistic “investors” have been throwing a ton of money into a relatively small number of big tech companies. In anticipation of… well, miracles. That simply aren’t manifesting at least in the way and extent to justify all this expectation of creation of great wealth. I’ll just mention the looming specter of disruption, especially in regards to the labor market. Some folks are concerned, and watching the situation closely. For now, the worst thing that has occurred are a growing number of investors becoming nervous over spectacular valuations with no huge results (involving profits) in sight.

I call the market a wealth machine (again, it’s “wealth”), given how it is treated. Make the right bets, and you are rewarded, sometimes handsomely. But the bets can be quite technical, based on trends that span at times very small intervals of time. And in fact is propped up by a number of gimmicks: stock buybacks, margin debt, option trading… and add to this list the reality of something like over half of all trading is now performed by computers.

It is a democratic system… as long as you have enough money (including access to debt). And ends up being a matter of a relatively small section of the population that is involved (and able to benefit). It is estimated that the top 10% of Americans hold up to 90%, or even higher, of all stocks. For the top 1%, the percentage is something like half of all stocks.

The Mirage

This is the unreality of the dominant mainstream narrative, directly and indirectly presented via the media and statements by the government and elite. Although this narrative is diffuse, without a fixed form, it is based on a kernel that goes something like things (the state of affairs of society, of America) are fine. Things are fine, nothing to be overly worried about, go about your everyday life without concern. If there is anything to be concerned about it’s how to spend one’s time and how to spend one’s money – involving choices in the context of a consumerist society.

And so it appears, despite a myriad of warning signs and worrying trends, that things in America are ok. Perhaps there are more “bumps” and looming problems than previously seen, but life is workable. Most people have jobs (ahem – see LISEP reference above), are housed, can buy food and generally obtain necessities if not some luxuries – although for a large portion of the population the prices for many things have been rising and some prices (like for cars) are reaching WTF-level, accompanied by an increasing reliance on debt to keep one’s lifestyle (relatively) intact.

Ah yes, back to debt. Note how it keeps on coming up.

Media and Digital Technology

Much of the unreality that has been discussed so far has been in terms of narrative and data skewed by narrative. It is what is presented in mainstream news and in dominant stories such as the American Dream (such as dished out by the two main political parties). But there is another form of unreality that is even more insidious given its scope and effects. And that is the torrent of images and sounds that we are immersed in, akin to the air we breath. Emanating from the countless screens, both large and small (i.e. “smart” phones) and which now literally envelop most of us (so that they now constitute a major part of our physical environment), they capture our attention and shape our thoughts. It is a literal torrent, as if we expose ourselves, “willingly” (the quotes relate to a whole other discussion), to the direct blast of water from a fire hose.

The Matrix

The range of this onslaught is in itself overwhelming. Even “unedited” video footage is mediated (“framed” in some way). And much of even supposed raw footage involves some sort of performance. And it is ubiquitous, in location, courtesy of cell phone technology, as well as time. It is a 24×7 barrage that, if considering TikTok accounts for example, involves millions of channels. The onslaught is simply staggering in its dimensions.

This torrent includes the glut of entertainment, where the choices are… well, staggering. Just about anything you wish to view is available just about anywhere and at any time. Many of us are immersed in all manner of dramas – our favorite shows! And much of it is not just ubiquitous but free. Free, that is, courtesy of all the ads. And this is yet another dimension rarely addressed. The sheer onslaught of idiotic skits and pseudo-dramas – many times harnessing the vast resources of the media industry – designed to hustle us, to inject references to products and brands and suggestions as to how they might enhance our lives.

As far as the ads go, my take is that it constitutes an assault on cognition itself – a prime ingredient to a population becoming not just stupefied, but stupid.

It is as if we have successfully replicated the situation described by Plato in the Allegory of the Cave, with many physical surfaces, not just screens, effectively converted into the cave walls upon which illusions are displayed. As far as The Matrix goes, there is no need for having to be literally “jacked in.” Especially as much of that torrent is designed to capture our attention, in a process that is nothing less than a form of addiction.

And now we have the input of AI, including an onslaught of “AI slop” to “enhance” our media offerings.

(Wow! Can’t help but insert a comment here on the irony of the so-called progress that is the result of advances in digital technology: a population sated and bloated not just on stuff – heretofore cheap – but stimulation.)

Encapsulated Life

Our everyday life, for the majority of the population, is without hyperbole drenched in this torrent of electronic stimulation. It is a major component for what I call Encapsulated Life. A life that is effectively buffered/cut off from the outside world, from the majority of fellow citizens (let along humanity), and from reality itself. This component works in conjunction with physical components (like much of our housing) to seal ourselves off.

This buffered life has another dimension, which involves a subtle form of unreality. Namely, for the majority, the complete lack of acknowledgement/comprehension of what supports this life. It’s simply taken for granted that we have access to all the world’s resources. And besides material resources, there is the effort of countless human beings who are otherwise invisible (and in many cases working in harsh, even toxic, environments). A vast process (aka The System) making our enviable life possible.

Add to the preceding the immense cost of all this. A cost that until recently has been invisible, but that is now starting to become apparent (see Reality Will Have Its Due) with recent inflation and high prices.

The “Smart” Phone

This preeminent example of modern computing and communication technology has become the main force behind the explosion of digital tech in scope and penetration in our society. A few elements of this technology are problematic as relates to the theme of unreality.

For one, there is the “dopamine loop.” This is a more formal way of describing the addictive effects of constant usage, including constant notifications and clicking on “likes” and links – for more more more. And the hypnotic effect of being blasted by imagery that is designed to capture one’s attention (many times with the side effect of forcing ads on that captured attention). The end result is a form of capture.

This leads to the idea of “distancing.” This is akin to the buffering/sealing off component of Encapsulated Life. It is literal. We see it in so-called zombie behavior, with people around us oblivious to the surrounding world and human beings.

And there is the concept of the “reality bubble” (or silo). The attention so captured is further being managed by algorithms that are constantly on the look out for favored categories of content (what a user tends to click on for example). In this way we are steered toward “realities” that can include not just products or lifestyle choices, but political beliefs. These algorithms are now being supercharged by AI technology. (comment: progress!)

This is a huge and very important topic in itself. For now it will be left that these devices are single-handedly deepening the condition of unreality. And are leading to subtle, negative consequences for society (such as the rise of mistrust and wariness towards those around us).

Yet Another Instance of Unreality

… and perhaps the most pernicious: the belief/expectation that things will continue pretty much as they are now – with both the status quo and trends. This contains the implication that there are no serious repercussions to things such as the exploding deficit or that our lifestyle is dependent on resource extraction with problematic (even toxic) effects on other nations and the planet itself. This overall belief can be captured in specific instances, as found in the following statements (a list that is not exhaustive):

- The United States will continue to be the most powerful nation on the planet (and history)

- The surging (exploding) deficit – and debt – will not hinder or cripple it in any way, especially in connection with the next item:

- The dollar will remain the world’s most important reserve currency

- Speaking of debt – the consumer will be able to maintain their lifestyle with continued – and expanding – reliance on debt

- The penultimate wealth creation machine – the US stock market – will despite a few stumbles now and then will always march up to new heights (that is, it will not see anything like a major crash that leads to an extended bear market, as has occurred several times in the past)

- Technology, especially digital tech, will continue to innovate and bestow upon us, everyone, all manner of benefits – and any negative side effects can just be shrugged off (see “stupid” and “stupefaction” a few points below)

- That the exemplary technology of AI will lead to not just benefits, but miracles – benefiting all humans

- The wealth gap that has widened, though a bit troublesome, remains something we can live with

- An increasingly stupid and stupefied populace will be able to come together and deal with any major problems that might arise (how about, for instance, an emerging water crisis in the Western US)

Debt

Debt has been mentioned a number of times in the preceding sections. I make the case that debt is one fundamental reason why we haven’t fully seen the SHTF. It is, in other words, a major (even “the” major) support in keeping up the appearance of normalcy, there is nothing to be overly concerned about, etc.; it is a primary force in staving off reality.

A sketch of this debt includes:

- The federal debt that has now surpassed $38 trillion (projected to reach $39 trillion in April 2026); this does not include many trillions more in

- Total debt for consumers reached $18.8 trillion early 2026. This includes

- $1.28 trillion in credit card debt (and counting)

- Plus over a trillion for auto loans and student loans

There’s more: how about all the margin debt (debt used to buy stocks on margin). And private credit. Which, btw, is showing worrying signs of strain, with an echo of the sub-prime crisis of the GFC.

What is the unreality of all this? It’s not even so much in the staggering totals, but in the nature of debt as essentially borrowing from the future. The unreality is the magical-like thinking that somehow in the future all this debt will be adequately dealt with.

Reality Will Have Its Due

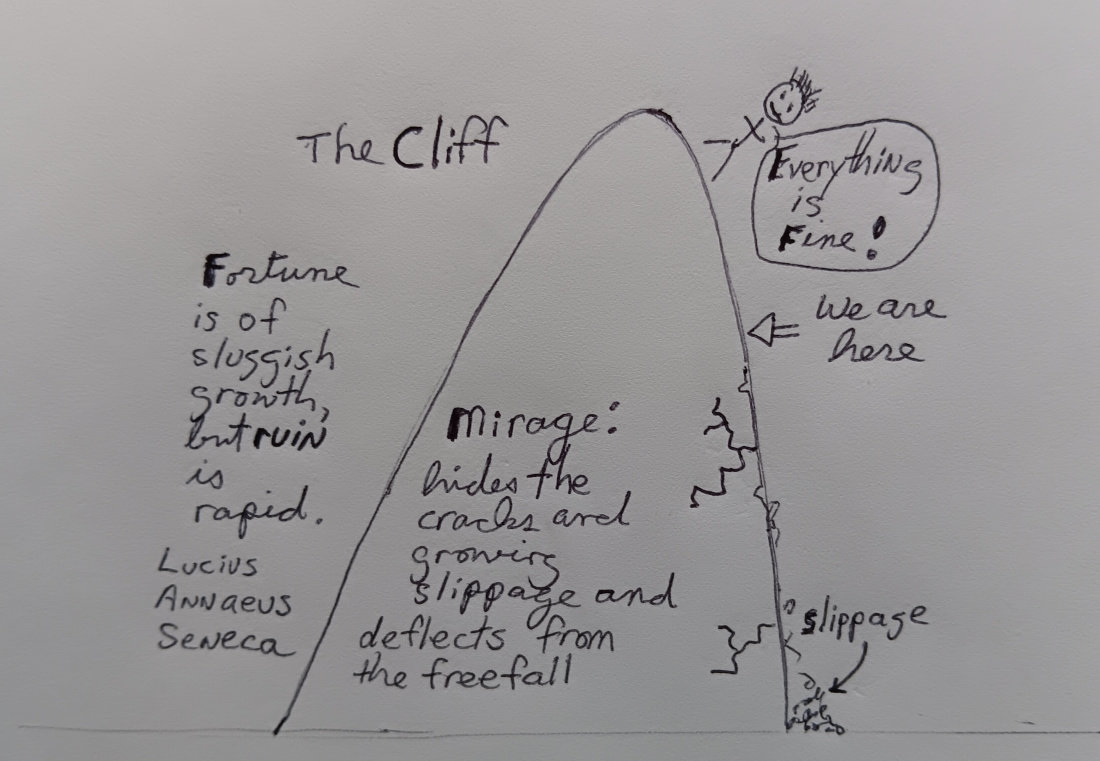

Again, it’s not that we are beset by unreality – it’s the expanded scope, and how it has so thoroughly insinuated into society and our lives. And this In the face of growing/widening cracks and accumulating warnings – some now flashing bright red. And this includes the ever rising level of debt that as I just laid out is one of the props of support keeping the whole thing from collapsing outright (and btw this includes our national debt continuing to be financed in the form of Treasuries). It’s as if we are at the edge of a cliff, and in fact beginning to lose our footing – see image at the end of this post.

Btw, I have not delved into the political sphere, which is rife with unreality in all sorts of ways. The OG is only one aspect, albeit prominent given his outrageous performance as the “leader of the free world.” But overall, the whole political process has become an unnerving performance, complete with insults and bullying and tons and tons of bs. Unnerving because it (political process) is unable to squarely deal with all manner of problems on a national scale, with the surging deficit and looming Social Security shortfalls as only a few examples.

Yeah, things look workable doe now. But things are slipping. And all the bravado and chest beating, the miracle of the Magic Money Machine and reliance on a mind-boggling pile of debt that for now help keep up the appearance of normalcy (The Mirage) cannot prevent the whole thing from eventually imploding. And the main force that is threatening us isn’t some enemy – external, such as Iran, or internal, such as Democrats or domestic terrorists – but reality itself.

Wow, that escalated quickly – way beyond initial intention. And this discussion is, as I said at the top, just a sketch. It has allowed me to collect various disparate observations and analyses, and bring some clarity to a gut feeling. Namely, something has been, and is, very very off in this country…

Part of this gut feeling has been an ongoing sense of unreality that has seeped into and encroached upon American life. It’s as if we can glimpse the edge of a cliff TO DO towards which our society is hurtling, much like that coyote (Wile E. Coyote) running after the roadrunner (which btw we can see literally with many drivers on our roads pressing hard on the gas pedal).

And now we are in the midst of a major war, and an undeclared one at that. And with an opponent who, though beaten up after some weeks of relentless bombing, still appears to have a number of tricks up its sleeve, including the ability to launch sophisticated ballistic missiles every day to Israel (among other places). The rhetoric of our superiority, the mounting cost (which will be effectively borrowed and added to an already large deficit), and so on, will as I see it have one major and lasting effect on the country (even if soon we are able to truly declare “we won”) which is that we have effectively accelerated our descent into The Decline.

I will end with a quote, from a poem by William Butler Yeats (which introduces Hedges’ Empire of Illusion):

We had fed the heart on fantasy,

The heart’s grown brutal from the fare.

TO DO image showing Wile E. Coyote past the edge of the cliff (drawn as Seneca’s Cliff)

{kind=link}