Something big is going to happen…

Whew… after attempting to keep up with all that is going on, I feel exhausted! It’s similar to when I had a blog on hardscrabblefuture.com some years ago, in response not just to the first Trump presidency (what his win signified) but other events and trends that pointed to an uncertain, and problematic, future. I eventually abandoned it from the relentless onslaught of these events and trends. It was simply too much, and to just enumerate each event and crisis with at least possible significant implications became pointless. The forest was lost, and instead I was lost in the trees.

The onslaught has only changed in scale. Trump’s second term has been one vast disruption, from massive tariffs/ trade wars to aggressive use of ICE and the National Guard of some states. And now we have the longest (or close) government shutdown in history (with many side effects – the cancellation of SNAP benefits being one of many). But all this chaos and divisiveness are only part of the story. There is the vastly overvalued stock market in the midst of a bubble (AI), whose popping could be a major disruption in itself, the rising number of consumers experiencing financial distress (with record, and rising, debt levels and delinquency rates)… and that’s just for starters.

In the face of all this there is a question that keeps popping up: how long can this go on? That is, how long can this situation continue before… the cracks become full-blown breakages. Beyond the low levels of consumer confidence (such as marked by University of Michigan) and political polls that by themselves are flashing warning signs, there is less quantifiable and anecdotal evidence that a growing unease is taking hold in the country. In various contexts you can hear references to things like a major market crash or a financial crisis (with private credit for example), or a clash with ICE leading to deaths and further disturbances… or even to a new civil war (recent polls give results showing anywhere from 40% to 57% believe such a war is likely or somewhat likely). As such, we can liken our situation to a precarious teetering on a…

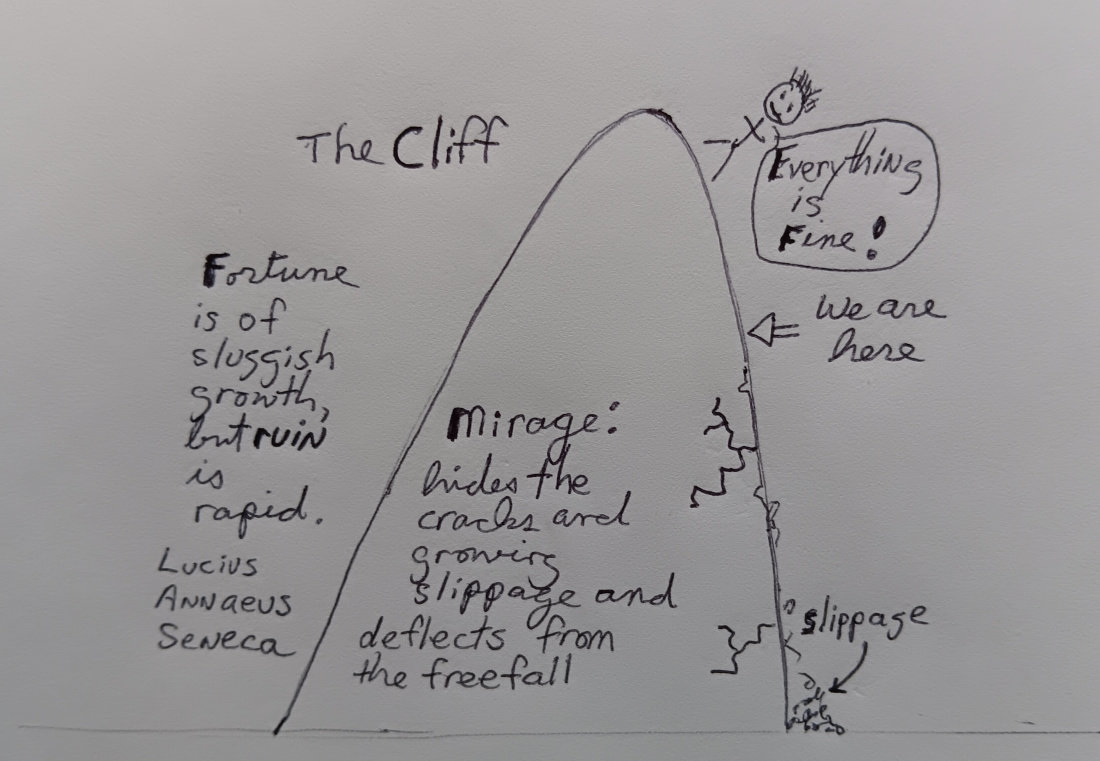

Precipice

This idea is captured by the drawing at the top. For one, even as our society begins to slip over the edge, we keep getting bs Mirage talk that things aren’t so bad (“Everything is Fine!”), or from some quarters that the situation is actually pretty good. Talk about a perfect instance of hyper-normalization. Yes, it can be argued that society isn’t in free-fall, that nothing has fundamentally broken (at least so far). Despite all the warning signs, some described below. To be sure there have been “slippages”, but no out-and-out catastrophe. Which encourages a surreal hyper-normalization that allows the population to go about their daily lives. But I argue, along with others, that we go about our daily lives teetering at the edge, beyond which… lies something… not so good.

There are a number of questions. For one, what exactly is this something? Other than to speculate that some people could get killed or that a lot of “wealth” evaporates, I really can’t say much. I have the more metaphorical idea of Wreckage. There will be some sort of mess in the wake of the SHTF, and an ancillary question as to how it will be cleaned up. In connection with the theme of Decline, I can only speculate that whatever occurs will only reinforce the condition of Decline, and that any attempt of recovery will probably will be haphazard at best. If nothing else, we won’t have the money for it.

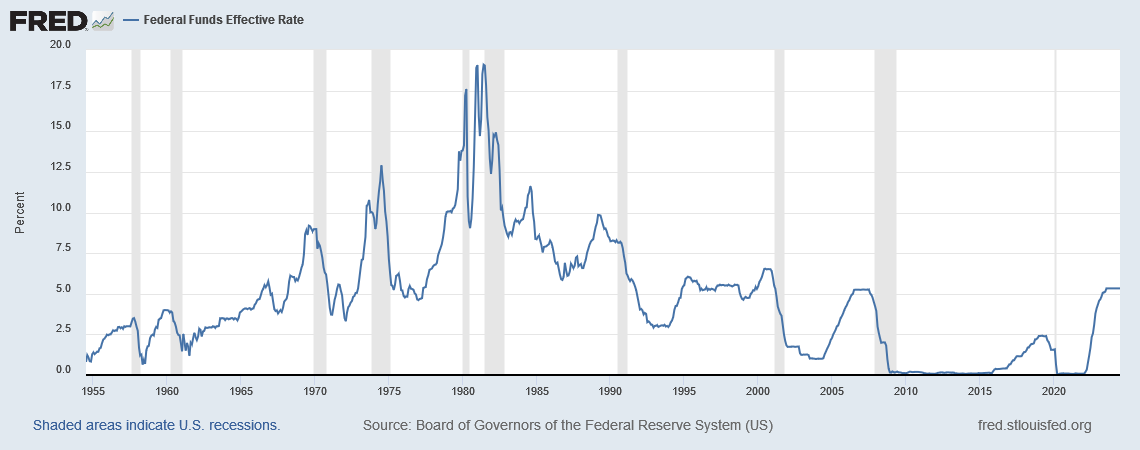

And there is the question of what actually sends us into free-fall. One thing I have encountered is the idea that collapse is not an event, but a process. Perhaps (or most likely) we’ll see a series of major slippages, as it were, rather than a single dramatic catastrophe. A series of events that take place over a period of time. I still see a high possibility of something major in the near term, like a financial crisis coupled with at least a severe market correction, but I also see there will be attempts by the government and the Fed to offset the pain involved – in fact, we can see such attempts being put in place now, with the Fed halting QT at the start of this December and the government blasting the economy with the equivalent of stimulus at the start of the new year. This is “kicking the can down the road,” which we have been doing for some time and is itself a major aspect of The Decline. But again the question comes up: how long can this continue.

Not in doubt are a multitude of trends and conditions that constitute the “edge of the cliff”: a slowing economy, a market that is extremely overvalued and in the grips of a bubble, a financial system showing worrying cracks, a shitload of debt (that continues to increase), extreme political and social polarization, as well as other things. All combining to form what some refer to as a “toxic cocktail” and given more detail in the following sections.

The Unraveling Economy

What, some would ask. are you talking about? We’re seeing “healthy” GDP numbers! Q2 GDP has been recently revised up to 3.8%, a big rebound from the slight decline in Q1. And, although it hasn’t been confirmed yet, Q3 could possibly be higher. Hell, corporate earnings have come in for most part acceptable, if not pretty good. And then there is the stock market making record highs (which gets its own section, that follows; not least of which because the market has all but disconnected from the real economy)!

And yet… square such good news with a sampling of data points that follow:

For one, we are seeing a large number of store closings (in the thousands) and corporate bankruptcies. The latter is at a 15-year high. So far through October, there have been 655 such bankruptcies (verses a total of 687 for all of 2024). So-called mega bankruptcies (assets greater than $1 billion) are particularly high: 17 in the first half of the year.

Many franchises, restaurants and retailers, have stated missed earnings and/or given warnings. McDonald’s, Chipotle, KFC, IHOP, Subway… Home Depot, Target… the list goes on. Burger King is closing around 370 outlets, Denny’s 90, Wendy’s a bunch more. Of course there is always churn, but this time around we have the situation of fast food workers unable to afford the food their place of work offers (other than an occasional meal). A number of CEOs have raised alarms over an overall pullback of low-income as well as a portion of middle-income households.

It’s still not clear as to the effects of the tariffs and illegal immigration crackdown. One thing we are hearing in regards to the crackdown are from farmers who are concerned at a sudden lack of workers to work the fields. We hear something similar from the construction sector. It might take awhile to have a full effect, but these developments are sure to be inflationary.

One main component of the economy is the labor market, which can be summarized as “softening.” Until recently the market could be described as “low fire, no hire,” but that appears to be coming to an end with an onslaught of recent layoff announcements. Large companies such as Meta, Amazon, Walmart and Microsoft are cutting many thousands of jobs.The recent report put out by Challenger, Gray and Christmas gives a figure of 153,074 job cuts for October, the highest number for any October since 2003. 2025 has been the worst year for layoff announcements since 2009 (GFC era).

Given the GDP numbers, the cheerleaders are chortling “recession? what recession?” But an analysis by Moody’s Analytics has concluded that 22 states are in a recession or at high risk of one. A number of measures relating to manufacturing indicate contraction. The Conference Board’s Leading Economic Indicators is in contraction, and has shown 16 months of consecutive declines. How about the trucking industry, with leaders stating they are experiencing a “freight recession.” This doesn’t exactly paint a rosy picture of the economy, despite the GDP numbers.

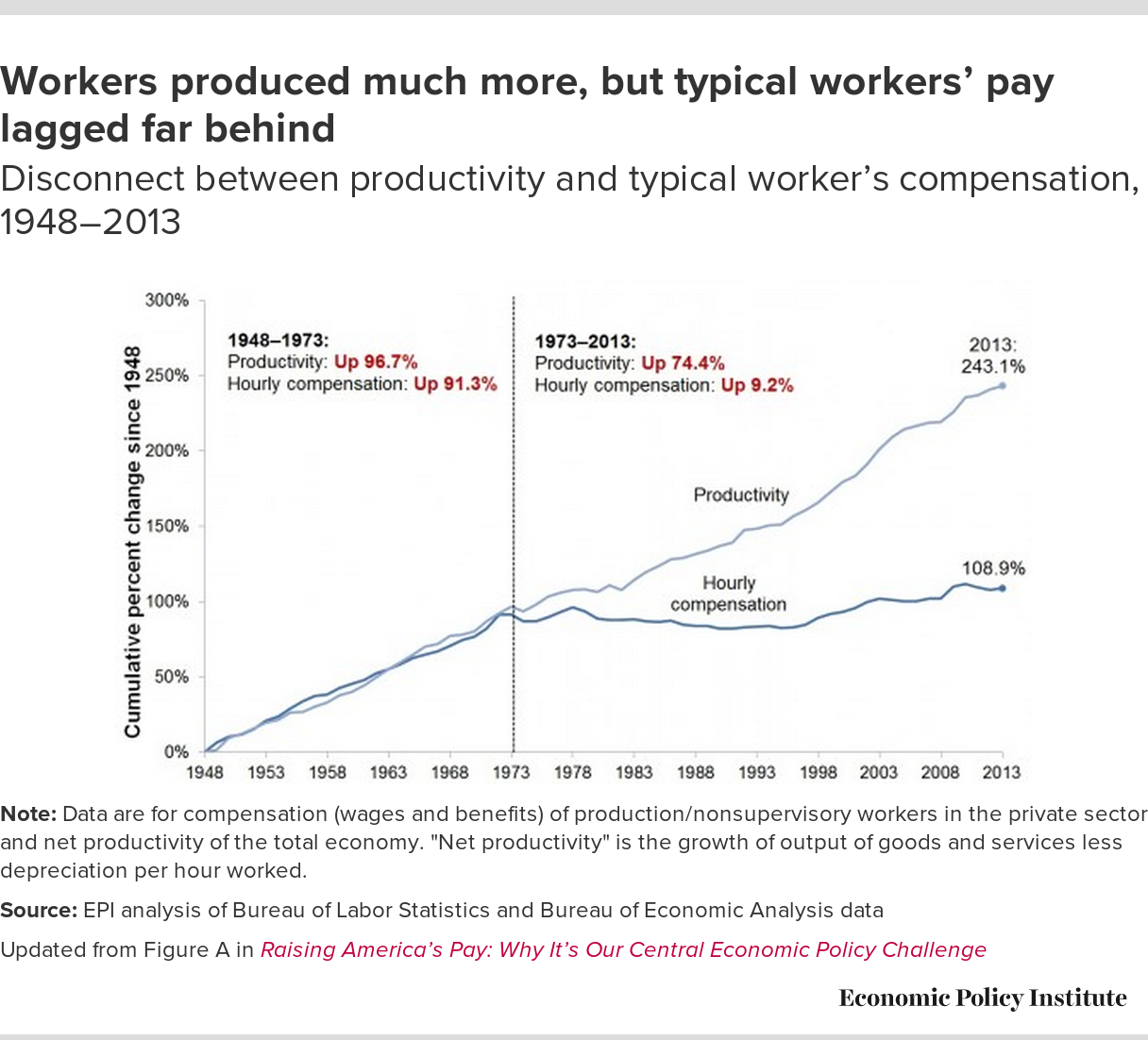

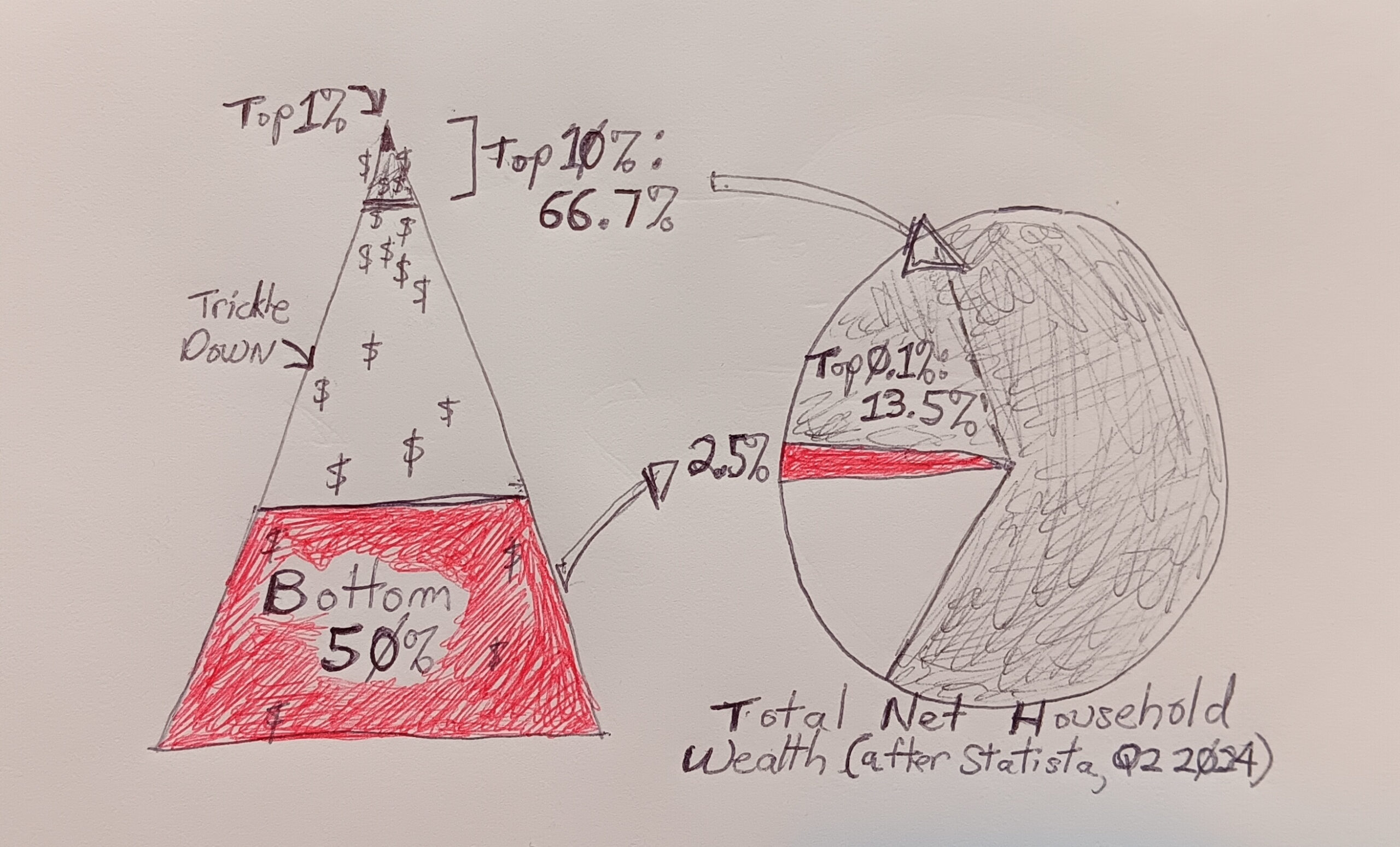

One major thing to keep in mind concerning the GDP number, is that about 2/3rds of it comes from consumer spending (not from production of actual goods and services). But it has been found that the wealthy account for the bulk of that spending (Moody’s Analytics and others). Specifically, the top 10% income tier account for almost 50% (half) of total consumer spending; the top 20% of earners are behind a shocking (for some of us, anyway)two thirds of all US spending. While the bottom 80% saw their share slip to 37%, down from 42% before the pandemic.This is a pretty lopsided state of affairs. But another important thing to keep in mind is that much of the “wealth” of the top tiers comes from… stocks.

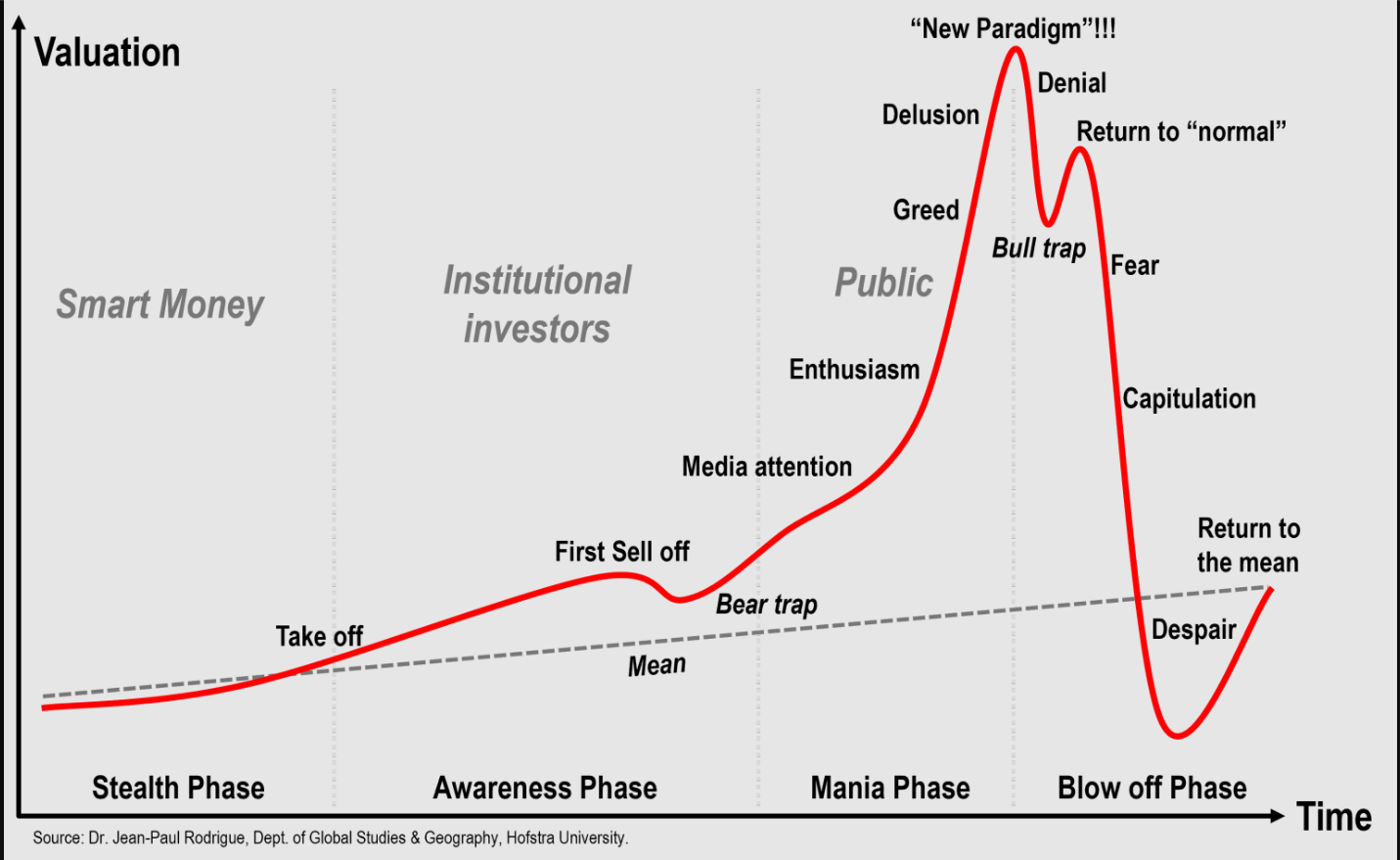

The Stock Market (Bubble)

In the past you would mostly hear the phrase “we don’t know we are in a bubble until it pops” from the MSM. This time, though, quite a few voices aren’t beating around the bush, including none other than OpenAI’s Sam Altman. We are in a bubble, and it is based on AI. And there is a sort of mania that has developed over AI.

Starting out, the market is extremely overvalued. Using the Buffett Indicator as a kind of barometer, the stock market as a whole is solidly in high risk territory, with the total market cap 219% of the value of the US economy (that’s over 2x the size of the real economy). There are other measures, such as the S&P 500 Shiller CAPE ratio, which is also at a level setting off alarm bells. The point being made is that such peaks have always preceded major declines.

There are other worrying signs. The market is dominated by only a handful of stocks, many in the tech sector and tied to AI. This lack of breadth has been a major red flag in the past.

Although there are a number of problems relating to the current AI rollout, a few can be mentioned. For one, there is simply very little to show in terms of ROI. There is some nervousness over this, especially with all the money being poured into data centers (which leads to a separate discussion). There is also growing awareness of the quirks and limits to the current AI approach (LLM – large language models). Then there is the, to some alarming, amount of circular financing. This is where some large firms, such as Nvidia and Microsoft, invest in AI startups, which then… use the money they receive to buy chips and cloud services – from the investors. It appears there is a lot of economic activity. But in reality it’s basically a kind of mirage. And such activity was a feature of the dot-com bubble.

One big element in the current market’s rise and a major red flag is the rise of margin debt. It has now reached over $1 trillion. … not far behind credit card, auto loan and student loan debt. As is “well known,” such debt can be instrumental in market surges, but conversely act as a major accelerant in declines/ crashes. This level of this sort of debt equates to a very high level of risk.

Financial Sector

The banks are said to be in good shape. Despite the rising delinquencies, among other problems (such as the huge level of unrealized losses). And a chunk of their loans are problematic, if not toxic. Debt related to credit cards and auto loans, for one. But also commercial real estate (a topic all its own).

But there is a big problem that has been hidden, swept, as it were, under the rug: private credit, involving several trillion dollars. Regular banks are encumbered with all sorts of regulations that are in response to irresponsible practices that have led to problems and crises, the biggest one in recent history being the GFC. Solution: create a sector comprised of “shadow banks,” which are not subject to those regulations (at least in ways that matter). But these entities, such as BlackRock, also entail risk. Lots of risk.

A recent example is that of a firm called Renovo (“home improvement”). It was bankrolled by BlackRock (largest asset management firm in the world). Not long ago the loan was considered 100 cents on the dollar. Just recently, they filed for bankruptcy (Chapter 7). And just like that, the loan was said to be a 100% loss (0 cents on the dollar), at $150 million. Huh… The thing is, shadow banking involves a lack of transparency, the kind that is mandated for regular banks. Given there have been bankruptcies with other firms, notably in the subprime auto space, there is a growing nervousness over the question as to what else is out there.

This sort of thing could be a trigger to a crisis, similar to the subprime mortgage meltdown in the housing bubble.This is a developing story… to be continued.

Reliance on Ever-Rising Levels of Debt

in all sectors: government, consumer, and corporate.

As of October federal debt reached $38 trillion. As comparison, as of late 2025 Q2 nominal GDP is given as $30.5 trillion. The interest on this debt is ballooning as well, and if the third-largest item in the federal budget. It is behind only Social Security and Medicare, and is larger than what is budgeted for national defense. The thing is, this money (interest) is not available for other things. Um, like health care… Adding to the alarm is the acceleration of the increase of this debt. It is now the case that this debt is increasing by $1 trillion in time period between 71 to 100 days. You can hear that question: how long can this continue?

Total consumer debt has now reached a record (just about all the numbers in this section are in record territory) $18.4 trillion. This includes:

- $1.21 trillion for credit card debt; new debt incurred subject to very high interest rates

- $1.66 trillion of auto loans

- $1.65 trillion for education loans

These are all seeing an uptick in delinquencies. For student loans, 10% is considered to be “seriously delinquent.” And will soon lead to actions like wage garnishing.

All of this is problematic, and unsustainable.

Political Paralysis, Divisiveness

The government shutdown is only the most prominent example of extreme polarization. The chief reason for Democrats withholding votes on the budget concerned expiring ACA tax credits. The abysmal state of healthcare in this country is a topic all to itself, but evidently many GOP politicians think because the ACA was created under liberal legislation it is fair game. The fallout of the shutdown also included the cancellation of SNAP benefits to millions.

I am not going to go very deep into the miasma of current partisan politics, but I am going to point out that Trump’s behavior is extremely alarming. Going after perceived enemies in such an explicit way (e.g. Comey) is, well, over-the-top. As is sending the National Guard to certain cities (which all happen to be liberal). One thing we can say he is succeeding in doing is stoking further divisiveness. Just what this country needs as the economy unravels.

One incident bears mentioning, though, and that is the recent murder of MAGA activist Charlie Kirk. Given the heightened level of polarization it has been construed as an assassination. Heated rhetoric from some MAGA folks including the president were pretty alarming, although it appears the worst of the anger has died down. But for a time it seemed, to me anyway, that the “knives had come out.” For hard-core right wing folks, the event cemented their view of liberals and progressives as enemies and to (for those on the hard right) America itself. Deserving to the “dealt with,” with the implication of violence.

Social Conditions (Unraveling)

A large number of American households have their back against the wall. A large percentage of Americans are expressing a decline in confidence in the economy, labor market, and expectations for the future, as captured in polling by the Conference Board and the University of Michigan.

One area particularly problematic is housing, with millions of renters behind on their rent. Also, foreclosures are ticking up. A significant portion of the working population is living paycheck-to-paycheck: the percentage varies by poll but several show close to two thirds (and apparently includes those making well in excess of $100k per year). Inflation is causing not just frustration but hardship for growing numbers. With food prices. And utilities. As well as costs related to cars, such as car insurance. And then there is healthcare (or rather, the lack of affordable quality healthcare). And the uptick in delinquencies and auto repos.

Another major element concerns the aggressive actions by ICE now aided by the use of National Guard in Chicago, as well as other cities, stirring up resentment in regions with large immigrant populations. Here’s an example of hyper-normalization: scenes of police-state tactics that are showing up regularly now.

Also to be included here in relation to the overall state of social relations is the already mentioned murder of Charlie Kirk. This has caused heightened distrust and anger. Perhaps not for the majority, but just about everyone was subjected to the heated rhetoric over the event. And most at least heard Trump using the event to demonize his “enemies,” the Democrats and other liberals.

In short, we have a society riled up by disparity (wealth, economic well being) and divisiveness. With a large chunk of the population frustrated, increasingly nervous… and glaring at one another.

At the Precipice – Nothing has broken… yet

There are hints of something up ahead… but we still are able to buy groceries and a plethora of stuff, albeit at higher prices. Many are still able to use and accumulate debt, although for a significant number this is increasingly for essentials. We even hear that spending this Xmas will exceed expectations (of course, this could just be bs cheerleader talk). Huh. I guess we will soon see.

But the thing is the economy is officially growing! No matter that about 2/3rds of GDP is consumer spending and the bulk of this spending is by the wealthy. Who are seeing their wealth surge… based on stock prices… in a market gripped by AI mania.

Hmm, a state of affairs propped by irrational exuberance and a lot of debt. But we see the cracks widen as well. And can hear the echos of slippage hitting the bottom, a long way below.

And so we’re left with that question How long can this continue?

For a growing number, the feeling of unease is tied to the uncomfortable answer,

Not a whole lot longer.