At the top of summer 2025, there is unbridled optimism among a portion of Americans: those at the top of the economic pyramid and others with the wherewithal to continue speculating in assets such as stocks and crypto. Aided by Cheerleaders in the MSM (see quote below), we get sentiment along the following lines: The economy is on a roll! Or about to take off! In any event, it is not in recession, and if one occurs it is still sometime off in the future. The tariffs are turning out to be a “nothing burger.” And so on. The problem is this optimism is not shared by a large number of Americans. And the economic data, if looked at in its entirety, is anything but a cause for celebration.

In the midst of writing this post, the BLS came out with their July report. Hmm, only 73,000 new jobs were created in July. But what was shocking were the large revisions for previous months. Now we are getting a dose of reality, with an average of 35,000 jobs created over three months ending in July (prior three months saw an average of 128,000), and a meek 1.2% average annualized GDP reading for the first half of the year (vs 2.8% for 2024). The markets initially reacted with a modest selloff. However, in the following days that selloff was erased and the optimism appears to be intact (and the Party continues, perhaps with some doubts creeping in). We’ll see how long it can continue. But given there has been as yet no “severe” reaction, I will continue as if this news can be treated as a “bump in the road,” and that the “great news” remains.

This quote of an analyst seems to encapsulate the prevailing view among those mentioned at the top of the post – those doing pretty damn well, damn any indication that the economy is anything but “robust:”

“No one expects the US economy to enter recession anymore.“

(Further update: as we continue into August, signs of doubt about the health of the economy are starting to pile up, some of them to be detailed below. However, the Party continues as the markets are still hitting all-time highs.)

The Great News Concerning the US Economy

So, what is the basis of such great news?

Well, look at the stock market! Back to making all-time highs!

And there is the historically low unemployment! Healthy amounts of new jobs are being created. The economy must be in great shape!

Perhaps there remains some pesky inflation, but the current rate is a lot less from what was seen in the previous year.

Oh, and we get a GDP print of 3.0 for Q2! Hallelujah!

So much for any major hit from the tariffs. The Party is intact!

But…

It’s kind of annoying to have to put in the effort to go through the above indications and give the details that are left out – either by laziness or intentionally – at least by MSM.

GDP and the Labor Market

Let’s get the GDP out of the way. I will have to give the MSM credit for stating at the outset that the import component to the calculation made a large difference. Namely, the large decline in imports (a negative factor in the calculation) was a major factor in that modestly high GDP print. Of course, this was a result of tariffs. Another factor has been the so-called front-running of the tariffs – economic “activity” that is misleading as to the true state of the economy. This included a build-up of inventory in anticipation of tariffs.

Mid-July the Federal Reserve put out its so-called Beige Book. This is the Fed’s take on the economy, which is broken down into 12 regions. In this report only 3 of the 12 regions showed growth, 2 of them only slightly. Not exactly an upbeat assessment.

And then there are all those jobs! Except, many of them have turned out to be a… mirage. We’ll put aside the chiding from LISEP, for example, who point out how a large number of these jobs are basically bs jobs – with wages not coming close to providing the wherewithal to cover the cost of living that an increasing number of Americans are having difficulty keeping up with.

But then the BLS came out with the July non-farm payroll numbers, along with revisions to prior months. And we got… a dose of reality. An average of 35,000 jobs created per month for the last three months (ending in July) should be the equivalent of being doused by a bucket of ice water. Also, the BLS notes that continuing claims remains elevated. This dovetails with anecdotal statements from a number of workers who report having difficulty finding work, especially in the tech sector. Corroborated by the University of Michigan survey, with an elevated % of those surveyed saying jobs are hard to find.

Inflation

Inflation, as measured by the CPI, has become, at best, subdued. There actually has in the last several months a slight uptick, such as in the related PCE. The latter could possibly be an indication that fallout of the tariffs has begun. One thing that many seem to miss, is that it was not realistic to think the fallout would be close to being immediate. A few voices, some major investors, pointed out that the effects would see a lag in roughly a six month time frame.

But one thing with the CPI and related, is that inflation as being broadly measured is flawed. Folks “on the ground” are sounding an alarm, based on grocery bills that only seem to climb as time goes by. If we just look at food prices, a more realistic picture emerges: in the first half of 2025, food prices have increased 12.5%, way beyond the more tepid readings. How could this be? The CPI is looking at all sorts of goods and services, a broad range – when, for example, did you last purchase a TV (whose prices have moderated)?

Stock Market

The stock market is, in a word, in a bubble.

There are a number of metrics that bolster such a view:

- The Buffett Indicator

- The CAPE Index

- Breadth

Tariffs

So much for all the deals that Trump boasted on concluding. At the time of writing, after the extensions ended, full-scale tariffs have hit close to 70 countries. Except some extensions are still in place. Such as with China. Which only means the full-scale tariffs are not yet in place.

A few people have noted that this on-again/off-again/abrupt change in course behavior makes it difficult for companies to make plans. This isn’t political: such behavior comes off as being fickle and, really, kind of dumb.

What remains to be seen is when the full-on effects of the tariffs hit. As yet, so far there has been no major problem with prices, except we have seen evidence that some prices related to imports are indeed rising. But you got to love it, more than a few analysts/etc have made the simple statement that the effects of the tariffs will take months to fully manifest. I say that because there seems to be a number of analysts/commentators/etc who appear to implicitly believe that the effects should have been seen almost immediately – and since they weren’t, well… time for those Victory Laps!

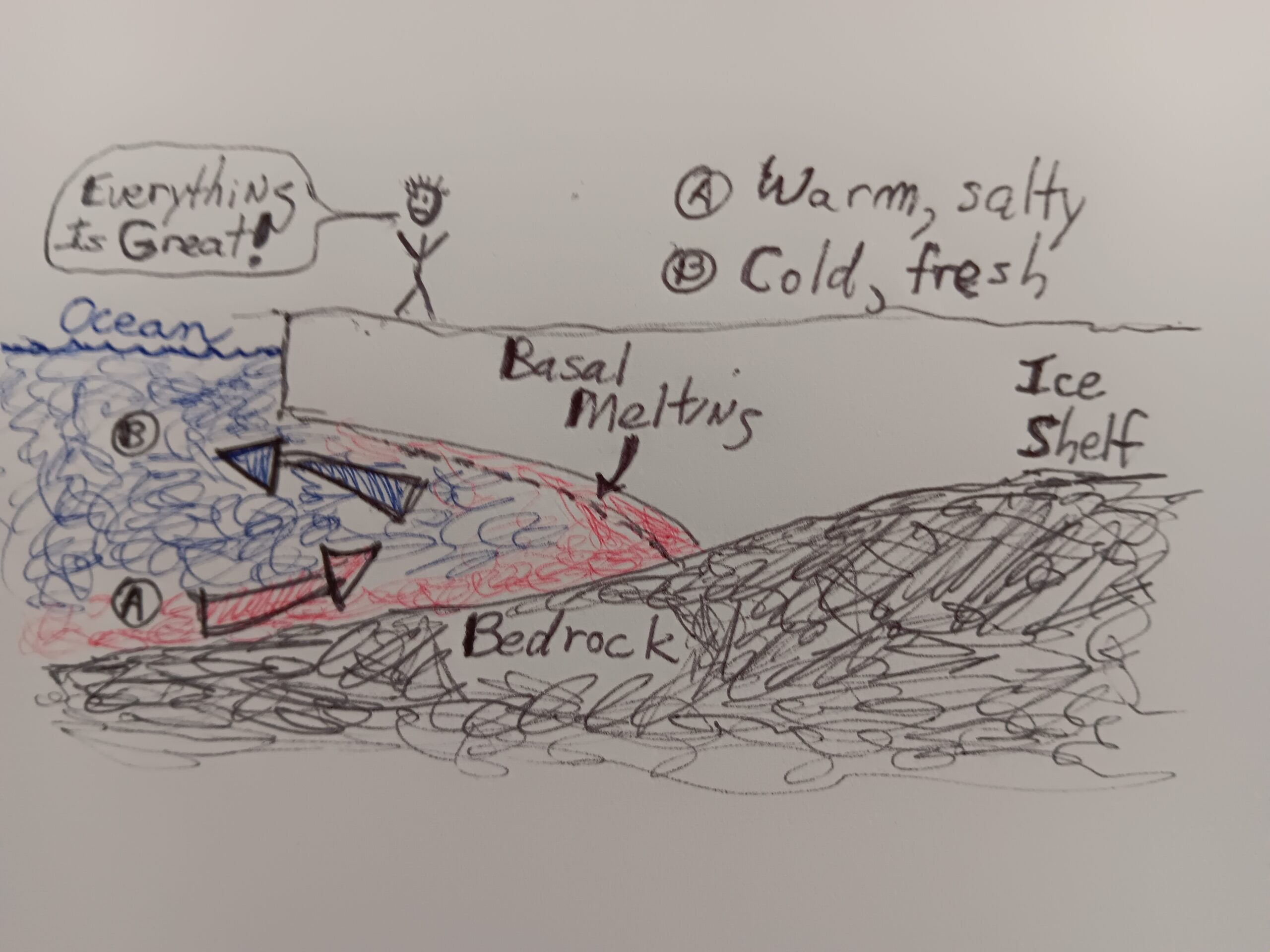

Analogy of Basal Melting

The image at the top is a simplified view of basal melting. The basic point of the analogy is that the deterioration of the ice shelf as depicted occurs from below, as warmer water (“A”) eats away at the underneath of the ice. And it does so out of view.

The Cheerleader type prancing about on the surface of the ice shelf thinks, wow, I don’t see any problem. Things must be fine! So much for the doomers. To rub it in the face of the latter the Cheerleader engages in a victory dance!

And that encapsulates much of what passes for expert analysis these days.

But out of direct view things are deteriorating. And direct view includes the data the majority of what the MSM chooses to present. The following is an enumeration of many of the signs that the economy is in a not-so-great shape. They interrelate in various feedback loops with each other, as well as other factors such large-scale climate patterns. They can be seen as cracks in the ice shelf.

To organize them they are grouped by categories.

Debt

In a word, we are drowning in debt. In all major sectors: government, consumer, and corporate. We’ll focus on the consumer:

- Total consumer debt, all categories: $18.4 trillion

- Credit card debt: $ 1.2 trillion

- Auto loans: $ 1.6 trillion

- Student loans: $ 1.6 trillion

That $18 trillion number, btw, is on par with the combined GDP of [ all of the ] Americas and the European Union.

Delinquency and Default

This category is basically Debt, but with a focus on increasing difficulty in handling the various types of debt.

This should be another wake-up call, akin to those recent job numbers, with credit card debt, auto loans, and student loan delinquencies approaching 2010 GFC levels.

One shocking element in this category is that the income group seeing the highest rate of rising delinquency are those making [ over $150k/ year – do do, check ].

Labor Market

The BLS has been having trouble reporting close-to-accurate figures for some time. They are reliant on surveys – two of them, the Establishment (business) and Household. The headline number given by the MSM is derived from the former.

One component of the labor market is the number of those with continuing claims.

Overall, some are calling the current situation “low hire, low fire.” The “low fire” part is deceptive –

Housing

The housing market has, in a word, stalled.

Affordability [ lowest on record ]

Commercial Real Estate

This sector is in big trouble. And very little of the “cracks” in this sector is reported by the MSM.

Sentiment

Overall, sentiment among Americans has reached levels that reflect their condition…

Cracks

The preceding gives a picture of an economy that is at best stalling. One that is facing all manner of vulnerabilities. Vulnerabilities that could, with the right trigger, lead to major events such as mass layoffs, a stock market crash, and a financial crisis (with banks imploding, for example).

The Victory Laps are basically a species of delusion. We are in the position of someone who believes, standing on a crumbling ice shelf, that what is beneath their feet is solid. Unable to see the deterioration that is otherwise hidden from their sight.